In this article we will discuss about:- Introduction to Neo-Classical Loanable Funds Theory of Interest 2. Assumptions of Neo-Classical Loanable Funds Theory of Interest 3. Supply of Loanable Funds (LS) 4. Demand for Loanable Funds (LD) 5. Determination of Rate of Interest 6. Cumulative Process and Monetary Equilibrium 7. Improvement over Classical Theory 8. Criticisms.

Introduction to Neo-Classical Loanable Funds Theory of Interest:

The neo-classical economists developed the loanable funds theory of interest which is an improved version of the classical theory of interest. According to the neo-classical theory, interest is a reward for the use of loanable funds and the rate of interest is determined by the demand for and supply of loanable funds.

Unlike the classical theory which deals only with the real factors of saving and investment, the loanable funds theory includes both real as well as monetary factors influencing the loanable funds and thus the rate of interest. The loanable funds theory was first developed by the Swedish economist K. Wicksell. Other Swedish economists, i.e., Myrdal, Lindahl and Ohlin, and the British economist D.H. Robertson refined the theory.

Assumptions of Neo-Classical Loanable Funds Theory of Interest:

The loanable funds theory is based on the following assumptions:

ADVERTISEMENTS:

(i) The market for loanable funds is a fully integrated market, characterised by perfect mobility of funds throughout the market.

(ii) There is perfect competition in the market so that one and only one rate of interest prevails in the market at any time.

(iii) Flexibility of interest rate is assumed so that it freely moves according to the changes in the demand and supply of loanable funds.

(iv) The theory is stated in flow terms, considering flow of demand for and supply of loanable funds per unit of time.

ADVERTISEMENTS:

(v) The theory assumes full employment of resources which implies constant level of income and output. In other words, an increase in investment, instead of increasing output, becomes inflationary.

(vi) Money is assumed to play an active role in the determination of the rate of interest and the banks adopt a stabilizing policy with the objective to establish monetary equilibrium.

Supply of Loanable Funds (LS):

There are four sources of the supply of loanable funds:

1. Savings (S*):

ADVERTISEMENTS:

Savings by households and firms out of their incomes form the major source of loanable funds. The neo-classical economists visualized savings in two senses. Firstly, savings are considered in ex-ante sense, as defined by the Swedish economists, i.e., savings planned by individuals out of the expected incomes. Secondly, savings are considered in Robertsonian sense, i.e., current savings are a function of past incomes. According to Robertson, savings are the difference between yesterday’s income and today’s consumption (S = Yt-1 – Ct).

In both these senses, savings are assumed to be interest elastic. There is a positive relationship between the rate of interest and savings; given the income level, as the rate of interest rises, the saving increases and vice versa. Like individuals and households, business firms also save. Such savings too are positively related to the current rate of interest. A higher rate of interest means higher cost of borrowing which encourages business savings as a substitute for borrowing from the market. But such business savings are generally invested by the firms themselves and may not constitute the loanable funds.

2. Dishoarding (DH):

Another source of loanable funds is dishoarding. Dishoarding means bringing out previously hoarded money and making it available for loanable purposes. At the low rate of interest, people tend to hoard money to satisfy their desire for liquidity and thus are discouraged to lend. But at a higher rate of interest, people are induced to dishoard money and increase the loanable funds. Thus, there is a positive relationship between the rate of interest and dishoarding.

3. Bank Money (BM):

Bank Money is yet another source of loanable funds. Banks advance loans by creating credit and thus add to the supply of loanable funds. Bank credit is also interest elastic; banks tend to lend more at higher rate of interest and less at lower rate of interest.

4. Disinvestment (Dl):

Disinvestment is also a source of loanable funds. Disinvestment means allowing the existing machinery to wear out without being replaced, i.e., not providing sufficient funds for depreciation. Thus, a part of firm’s earnings, instead of being kept in the depreciation funds meant for capital replacement, goes into the market for loanable purpose. Disinvestment is encouraged at a higher rate of interest.

Demand for Loanable Funds (LD):

The demand for loanable funds arises for three purposes:

ADVERTISEMENTS:

1. Investment (I*):

The major portion of demand for loanable funds comes from the business firms to meet their investment expenditure. The business firms need funds to purchase raw materials, capital equipment or to build up inventories etc. Investment demand for loanable funds is interest elastic; it increases with a fall in the rate of interest and decreases with a rise in the rate of interest.

2. Dissaving (DS):

Another source of demand for loanable funds comes from dissaving, i.e., from consuming more than the current income. People tend to borrow funds when they want to spend more than their current incomes. Such a kind of consumption demand for loanable funds arises mostly when the consumers decide to spend on durable goods like cars, scooters, T. V. sets, etc. Higher the rate of interest, smaller will be dissaving or consumption demand and vice versa.

ADVERTISEMENTS:

3. Hoarding (H*):

Loanable funds are also demanded for hoarding purposes. Hoarding means keeping money in idle cash balances. People have a tendency to hold cash balances to satisfy their desire for liquidity. A higher rate of interest discourages people to hoard and a low rate of interest induces people to hoard.

Determination of Rate of Interest:

The equilibrium rate of interest is determined when the supply of loanable funds (LS) and the demand for loanable funds (LD) are equal.

The components of the supply of loanable funds are:

ADVERTISEMENTS:

BM = Bank money;

I = I* – DI = net investment;

H = H* – DH = net hoarding.

Thus, according to the loanable funds theory, the equilibrium rate of interest is determined at the level where net saving plus change in bank money are equal to net investment plus net hoarding. In contrast, the condition for equilibrium rate of interest in the classical theory is given by the equality between saving and investment (S = I). Equation (5) also implies that market for loanable funds is in equilibrium, when S = I, BM = H and, in disequilibrium, when S ≠ I, BM ≠ H.

This means, that the loanable funds theory considers hoarding and dishoarding as a flow of funds that are zero when the total stocks of funds are in equilibrium and non-zero when the stocks are in disequilibrium. In contrast, Keynes’ liquidity preference theory is concerned with an asset holding equilibrium in which demand and supply of money are equal.

ADVERTISEMENTS:

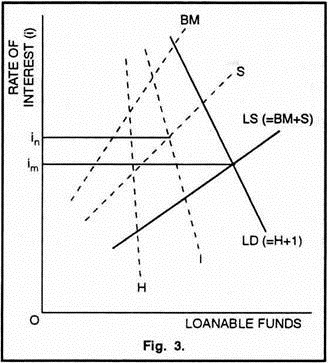

Figure 3 shows determination of the rate of interest according to the loanable funds theory. On the supply side, BM curve represents the supply of bank money and S curve represents the supply of savings. By adding BM and S curves, we get LS curve or the total supply curve of loanable funds which (like its component curves BM and S) slopes upward to the right indicating a positive relationship between the rate of interest and the supply of loanable funds; as the rate of interest rises, the supply, of loanable funds increases and vice versa.

On the demand side, H curve represents the demand for money for hoarding and I curve represents the investment demand. The LD curve, which is obtained by combining H and I curves, is the total demand curve for loanable funds. The LD curve (like its constituent curves H and I slopes downward to the right indicating a negative relationship between the rate of interest and the demand for loanable funds; as the rate of interest falls, the demand for loanable funds increases and vice versa.

The intersection of the LD (demand for lonable funds) and the LS (supply of lonable funds) curves gives the equilibrium rate of interest, i.e. Oim, according to the loanble funds theory. On the other side, the intersection of the I (investment) and the S (savings) curves gives the equilibrium rate of interest, i.e. Oin, according to the classical theory. It is to be noted that Oim (the interest rate according to the loanable fund theory) is less than Oin (the interest rate according to the classical theory). This shows that money no longer plays a passive or neutral role. It plays an active role in the determination of the rate of interest; its inclusion on the supply side causes the rate of interest to fall from Oin to Oim.

Natural and Market Rate of Interest:

ADVERTISEMENTS:

Wicksell distinguishes between the natural rate of interest and the market rate of interest. The natural rate of interest or the capital rate of interest refers to the rate of return on capital goods. It is that rate of interest at which saving equals investment.

The market rate of interest or the money rate of interest, on the other hand, is the rate of interest actually prevailing in the market. It is that rate of interest at which the demand for loanable funds equals the supply of loanable funds. In Figure 3, Oin is the natural rate of interest and Oim is the market rate of interest.

Cumulative Process and Monetary Equilibrium:

Wicksell’s cumulative process explains how the monetary equilibrium is achieved through changes in prices and market rate of interest, once a discrepancy arises between the natural rate on interest and the market rate of interest.

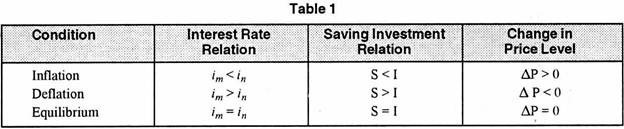

Monetary equilibrium requires three conditions to be satisfied simultaneously:

(a) The market rate of interest equals the natural rate of interest;

(b) Real investment equals real savings; and

ADVERTISEMENTS:

(c) The price level has no tendency to move upward or downward.

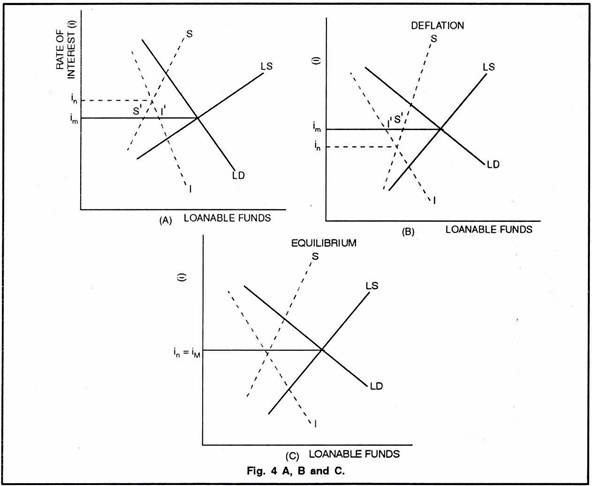

The monetary authorities have an important role to play in stabilizing the price level and restoring monetary equilibrium. Figure 4 and Table 1 illustrate Wicksell’s process through which the divergence between the natural rate of interest and the market rate of interest is removed and the monetary equilibrium is restored.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

(i) During Inflation (Figure 4A):

Market rate of interest is lower than the natural rate (im < in), saving is less than investment (im S’ < im I’) and there is a cumulative rise in prices (∆P > O). In such a situation, the demand for loanable funds tends to increase because the borrowers need larger funds to finance their investments.

On the other hand, the supply of loanable funds tends to decrease because the bank reserves are being depleted. In order to protect their reserves, the banks will raise the bank rate. This will, in turn, increase the market rate and bring it equal to the natural rate. Thus the monetary equilibrium is restored.

ADVERTISEMENTS:

(ii) During Deflation (Figure 4B):

The market rate is higher than the natural rate (im > in), saving is greater than investment (im S’ > im I’) and the prices are continuously decreasing (∆P < O). In this case, the bank rate will be reduced, which will lower the market rate and bring it equal to real rate. Thus, the monetary equilibrium is restored.

(iii) Monetary Equilibrium (Figure 4C):

Monetary equilibrium (Figure 4C) is established when the bank rate is such that the equality between the market rate and the natural rate (im = in), and that between saving and investment (S = I) is maintained. There will be no change in the prices (∆P = O) and no need of altering the bank rate.

Improvement over Classical Theory:

The loanable funds theory is an improvement over the classical theory in many ways:

(i) The loanable funds theory is more realistic than the classical theory in the sense that whereas the latter is stated only in real terms, the former is stated in real as well as money terms.

(ii) The loanable funds theory recognises the active and dynamic role of money in the modern economy, whereas the classical theory assumes money as a neutral or passive factor.

(iii) Unlike the classical theory, the loanable funds theory includes bank money as a component of the supply of loanable funds.

(iv) Contrary to the classical theory the loanable funds theory takes into consideration hoarding or inactive cash balances as an important factor influencing the demand for loanable funds.

(v) The loanable funds theory also distinguishes between the natural and the market rate of interest and explains why the market rate can be and normally is different from the natural rate.

Criticisms of Loanable Funds Theory:

The loanable funds theory is not a new theory, but only a modified version of the classical theory; in essence, it is the classical saving and investment theory. As such, it is open to the same criticism as the classical theory is. Though the loanable funds theory has improved upon the classical theory in some respects, it has its own defects too.

The main drawbacks of the theory are discussed below:

1. Misspecifications of Factors:

The loanable funds theory mis-specifies various sources of supply and demand for loanable funds:

(a) Not all savings come to the loanable market; some are invested directly by the households and the business firms.

(b) All dishoarding is not lent to others; some is spent by the dishoards.

(c) All investment or hoarding is not financed by borrowed funds; some part of it is financed by own funds.

(d) Funds are borrowed for many purposes other than investment, hoarding and consumption.

2. Unrealistic Integration of Real and Monetary Factors:

The neoclassical economists attempted to combine the monetary factors with the real factors in the loanable funds theory. But they did not succeed in this attempt. The two sets of factors are completely different in their origin, nature and impact and cannot be combined directly.

How can the real factors like saving and investment be combined with the monetary factors like bank money and holding of cash balances. A proper integration of the real and the monetary factors is possible through considering changes in the income level as attempted by Hicks and Hansen.

3. Unrealistic Assumption of Full Employment:

The theory is based on the unrealistic assumption of full employment. According to Keynes, less-than-full employment, and not full employment, is a normal feature of a capitalist economy. Thus, the theory fails to apply in the real world.

4. Unrealistic Assumption of Constant Income:

The loanable funds theory assumes that the income level of the community remains constant and the changes in investment have no effect on it. But the reality is that when the volume of investment increases as a result of a fall in the rate of interest, it leads to an increase in the income level.

5. Interest-Elasticity of Saving Over-Emphasised:

The loanable funds theory exaggerates the effect of the rate of interest on saving. Saving may not be so much affected by the rate of interest as suggested by the theory. Sometimes people start saving without any increase in the rate of interest. Sometimes people do not stop saving even if the rate of interest falls to zero.

6. Saving and Investment Equality:

The loanable funds theory implies that saving-investment equality (and also monetary equilibrium) is established through changes in the rate of interest. When market rate of interest is less than the natural rate of interest, investment exceeds saving. As a result, the market rate of interest increases which causes saving to increase and investment to fall.

Thus, equality between saving and investment as well as between the natural rate and the market rate is established. Keynes criticized this view and believed that it is the changes in income, and not the rate of interest, that brings about equality between saving and investment. When investment exceeds saving, income increases which leads to an increase in saving and thus making it equal to investment.

7. Indeterminate Theory:

Like the classical theory, the loanable funds theory is also indeterminate. According to Hansen, it does not tell clearly how the rate of interest is determined. In this theory, the rate of interest depends upon the loanable funds and the loanable funds depend upon savings.

But savings depend upon the income level. Income level depends upon the level of investment and the volume of investment depends upon the rate of interest. In this way we are caught in a vicious circle. The rate of interest cannot be determined with the help of this theory.