Read this article to learn about the top thirty-one frequently asked questions on the Forms of Market and Price Determination.

Q.1. State three salient features of monopoly market. Describe any one.

Ans. The three features of monopoly market are:

(i) A single firm i.e., only one seller or producer of the production in the market.

ADVERTISEMENTS:

(ii) No close substitute of the product.

(iii) Barrier to entry of new firms.

Q.2. Explain the features of a monopoly market. Why is the demand for a good under monopoly inelastic as compared to monopolistic competition?

Ans. The main features of a monopoly market are:

ADVERTISEMENTS:

(i) A Single Producer:

In monopoly, there is a single producer of the commodity in the market.

(ii) No Close Substitute:

There are no close substitutes for its product. It is the sole producer of a unique product.

ADVERTISEMENTS:

(iii) Restrictions on entry of new firm:

No other firm is allowed to enter the monopoly market due to legal barriers, natural barriers over the supply of raw material, economies of large scale production, goodwill of the monopoly firm.

(iv) Perfect knowledge:

It is assumed that a monopolist has perfect knowledge of market conditions. Under monopolistic competition, a number of close substitutes are available m the market so that the demand curve for a monopolistic firm becomes more elastic as compared to a monopoly firm which has no close substitutes for its product.

Q.3. Why is a firm under perfect competition a price.

Ans. i. Under perfect competition, price of a commodity is determined by the total demand and total supply in the industry.

ii. An individual firm can sell any quantity at this prevailing price decided by the industry.

iii. The number of firms under perfect competition is so large that a single firm has no control over the price and it has to accept the price determined by the forces of demand and supply.

iv. Further, the product being homogenous and with other sellers too selling at the same price, he is forced to accept the prevailing price of the product.

ADVERTISEMENTS:

v. A firm is thus a price taker under perfect competition.

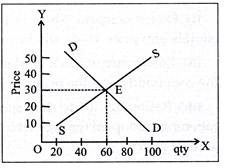

Q.4. How is price determined in a perfectly competitive market? Explain.

Ans. i. The price under perfect competition is determined by the total demand and total supply of the industry.

ADVERTISEMENTS:

ii. Each individual firm has to accept that price, since it can sell its product only at that price.

iii. That’s why a firm in a competitive industry is a price taker and industrial is the price maker.

iv. In the diagram below ‘DD’ and ‘SS’ are the demand and supply curves of the product for the industry which are intersecting at E. The equilibrium price determined by these curves is OP. Every individual firm can see any output at this price.

v. Thus the demand for a firm under perfect competition becomes perfectly elastic, because each unit of the commodity is perfect substitute of each other.

ADVERTISEMENTS:

Q.5. Explain the implication of ‘large number of buyer’ in a perfectly competitive market.

Ans. The implication is that no single buyer is in a position to influence the market price on its own because an individual buyer’s purchase forms a negligible proportion of the total purchase of the good in the market.

Q.6. Explain the implications of ‘large number of sellers’ in a perfectly competitive market.

Ans. The implication is that the proportion of total output produced by a single seller is so insignificant that the seller cannot influence the market price by his own actions by changing the quantity of output it produces. He has no option but to sell at the price determined at the industry level.

Q.7. Explain the implications of ‘freedom of entry and exit to the firms’ under perfect competition.

ADVERTISEMENTS:

Ans. The firms enter the industry when they find that the existing firms are earning super normal profits. Their entry raises output of the industry, brings down the market price and thus reduces profits. The entry continues till profits are reduced to normal, (or zero). The firms start leaving the industry when they are facing losses. This reduces output of the industry, raises market price and reduces losses. The exit continues till the losses are wiped out.

Q.8. Explain the implications of ‘perfect knowledge about market’ under perfect competition.

Ans. Perfect knowledge means that both buyers and sellers are fully informed about the market price. Therefore no firm is in a position to charge a different price and no buyer will pay a higher price. As a result a uniform price prevails in the market.

Q.9. Explain the implications of the feature ‘homogeneous products’ in a perfectly competitive market.

Ans. The buyers treat the products of all the firms in the industry as same. Therefore, they are willing to give the same price for all the products. A uniform price prevails in the market for all the products in the industry.

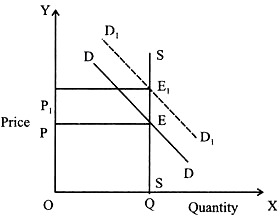

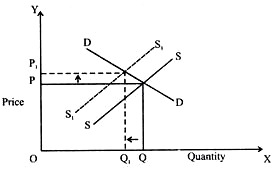

Q.10. Explain the effect of an increase in demand of a commodity on its equilibrium price and quantity. Use diagram

ADVERTISEMENTS:

Ans. i. An increase in demand will cause an increase in the equilibrium price as well as quantity of the commodity as shown in the diagram below:-

ii. In the diagram, DD is the original demand curve and SS is the supply curve. The equilibrium price is thus OP.

iii. When demand increased, the demand curve DD shifted to the right to D1D1. As a result the equilibrium price increased by PP1 and changed from OP to OP1. The equilibrium quantity also increased from OQ to OQ1

iv. The increase in demand thus increases the equilibrium price as well as equilibrium quantity of the commodity.

Q.11. Explain with the help of a diagram the effect of a decrease in demand for a commodity on the equilibrium price and quantity.

ADVERTISEMENTS:

Ans. i. A decrease demand causes a decrease in the equilibrium price and quantity as shown in the diagram below

ii. In the diagram, DD is the original demand curve and SS is the supply curve. The equilibrium price is OP. When demand decreased, from DD & moved to D1D1 and equilibrium price got reduced to OP1 and equilibrium quantity also got reduced to OQ1. Thus a decrease is demand decreases the equilibrium price as well as quantity of the commodity.

Q.12. How does an increase in income of the consumer affect the equilibrium price of a commodity?

Ans. i. An increase in income (Normal good) will shift the demand to the right, and due to increase in demand the equilibrium price and equilibrium quantity will increase as shown through the following diagram

ii. In the diagram, DD and SS are demand and supply curves intersecting at E. Due to increase in demand, the demand curve shifts to the right to D1D1 which intersects the supply curve at E1 and the equilibrium price rises from OP to OP1.

Q.13. There is no change in quantity supplied but demand rises, due to which price will also rise. Show how is it possible diagrammatically?

Ans. i. It can be possible only if supply is perfectly inelastic. When demand rises its curve shifts towards right from DD to D1D1.

ii. With that Equilibrium price rises from OP to OP1 and there is no change in equilibrium quantity.

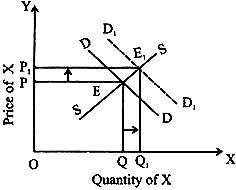

Q.14. If the price of a substitute (Y) of good X increase, what impact does it have on the equilibrium price and quantity of good X?

Ans. i. Since X and Y are substitute goods, an increase in price of Y will increase the demand for commodity X which will make the demand curve for X to shift towards right, as a result of which equilibrium price as well as equilibrium quantity of X will increase.

ii. In the above diagram DD and SS are demand and supply curves intersecting at E and OP is the equilibrium price. Increase in price of Y increases the demand for X; thus demand curve shifts to the right to D1D1. The new equilibrium point is E1 and the equilibrium price increases from OP to OP1. The equilibrium quantity also increases from OQ to OQ1.

iii. Hence increase in price of substitute good Y will increase the equilibrium price as well as quantity of good X.

Q.15. How will equilibrium price and quantity of a commodity be affected, when its supply decreases and its demand is perfectly elastic? Use diagram.

Ans. i. In case of a perfectly elastic demand curve decrease in supply will reduce only the quantity.

ii. In the diagram, DD is the perfectly elastic demand curve and the supply curve is SS. With the decrease in supply, the supply curve has shifted towards left from SS to S1S1

iii. There is no change in equilibrium price as it is same as before (OP), only the quantity has decreased form OQ to OQ1.

iv. Thus if the commodity has a perfectly elastic demand curve, in case of decrease in supply only quantity will be reduced but there is no change in equilibrium price.

Q.16. What will be the effect on equilibrium price and quantity, when there is an increase in the supply. Use diagram.

Ans. i. An increase in supply of the commodity will reduce the equilibrium price of the commodity and increase the quantity supplied as shown in the diagram below:

ii. In the above diagram DD and SS are demand and supply curves Corresponding equilibrium price is OP and equilibrium quantity is OQ. Upon increase in supply, the supply curve has shifted from SS to S1S1 .With increase in supply the equilibrium price has decreased from OP to OP1 whereas equilibrium quantity has increased from OQ to OQ1.

iii. Thus an increase in supply reduces the equilibrium price and increases the equilibrium quantity of the commodity.

Q.17. With the help of a diagram show the effect of decrease in supply on the equilibrium price and quantity of the commodity.

Ans. i. A decrease in supply of the commodity will increase the equilibrium price and decrease the equilibrium quantity as shown in the diagram below

ii. Now here the demand curve is DD and supply curve is SS, The equilibrium price of the commodity is OP and equilibrium quantity is OQ. Upon decrease in supply, the supply curve has shifted from SS to S1S1. The equilibrium price has risen from OP to OP1 and equilibrium quantity has decreased from OQ to OQ1.

iii. A decrease in supply thus increases the equilibrium price and decreases the equilibrium quantity of the commodity.

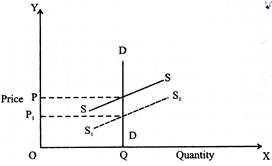

Q.18. What will be the effect on equilibrium price and quantity when demand is perfectly inelastic and supply increases? Use diagram.

Ans. i. An increase in supply will reduce the equilibrium price but the equilibrium quantity remains the same as shown below

ii. In the diagram, DD is the demand curve which is perfectly inelastic and SS is the supply curve. OP is the equilibrium price and OQ is the equilibrium quantity. On increase in supply, SS shifts to the right to S1S1. As a result, the equilibrium price comes down to OP1 from OP but the equilibrium quantity remains the same.

iii. Thus when demand for a commodity is perfectly inelastic, an increase in supply will reduce the equilibrium price only and the equilibrium quantity will remain the same.

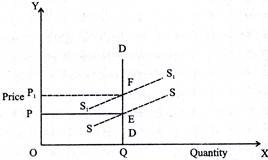

Q.19. What will be the effect on equilibrium price and quantity when demand is perfectly inelastic and supply decreases. Use diagram.

Ans. i. If demand is perfectly inelastic and supply decreases the equilibrium price rises but the quantity will remain same as shown in the diagram below

ii. In the diagram, DD is the demand curve which is perfectly inelastic. The supply curve SS is intersecting it at point E and OP is the equilibrium price. The new supply curve S1S1 is intersecting DD at point F. The equilibrium price has increased from OP to OP1. The equilibrium quantity is same as before i.e. OQ.

iii. Thus if demand is perfectly inelastic, a decrease in supply will increase the equilibrium price though the equilibrium quantity remains unchanged.

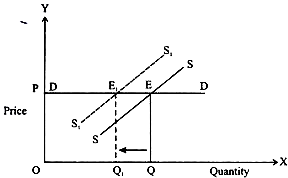

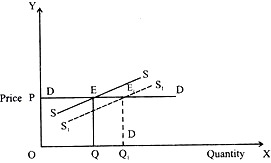

Q.20. Explain the effect of increase in supply on equilibrium price and quantity when demand is perfectly elastic. Use diagram.

Ans. i. When demand is perfectly elastic an increase in supply will increase the equilibrium quantity only, the equilibrium price remaining unaffected as shown in the diagram below: short answer type questions

ii. In the above diagram, demand curve DD is perfectly elastic. The supply curve SS is intersecting it at E. The equilibrium price and quantity are OP and OQ respectively. The increase in supply has shifted the supply curve SS to S1S1 which intersects the demand curve at E1. The equilibrium price remains the same (OP), but the equilibrium quantity has increased from OQ to OQ1.

iii. Hence in case of a perfectly elastic demand, an increase in supply increases the equilibrium quantity without disturbing the equilibrium price.

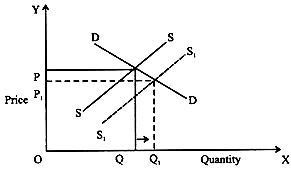

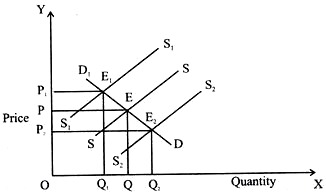

Q.21. Explain with the help of a diagram, the effect of shift of supply curve of a commodity on its equilibrium price and quantity.

Ans. i. In the above diagram, DD and SS are demand and supply curves intersecting at E. OP is the equilibrium price and OQ is the equilibrium quantity.

ii. On increase in supply i.e. rightward shift of supply curve the equilibrium price has declined from OP to OP2 but equilibrium quantity has increased from OQ to OQ2.

iii. If there is a leftward shift of supply curve (decrease in supply), the supply curve will shift from S1S1 to and new equilibrium price will become OP1 which is more than the original equilibrium price OP. The quantity supplied will be reduced to OQ1 from OQ.

iv. Thus in case of leftward shift of supply curve, equilibrium price increases but equilibrium quantity decreases and in case of rightward shift of supply curve, equilibrium price decreases and equilibrium quantity increases.

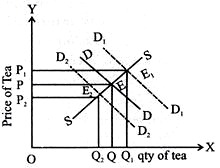

Q.22. How will a change in price of coffee affect the equilibrium price of tea? Explain the effect on equilibrium quantity also through a diagram?

Ans. i. Tea and coffee being substitute goods, an increase in price of coffee will increase the demand for tea and a decrease in price of coffee will decrease the demand for tea.

ii. In the diagram, DD and SS are demand and supply curves intersecting at E and OP is the equilibrium price. On increase in price of coffee, demand for tea will increase. Thus the demand curve DD will shift to the right to D1D1 and equilibrium price will increase from OP to OP1. The equilibrium quantity will also increase from OQ to OQ1.

iii. In case of decrease in the price of coffee, demand for tea will be reduced causing the demand curve DD to shift to D2D2. The equilibrium price for tea as well as its quantity will be reduced to OP2 and OQ2.

iv. Thus an increase in price of coffee will increase the equilibrium price as well as equilibrium quantity for tea and a decrease in price of coffee will decrease the equilibrium price and quantity of tea.

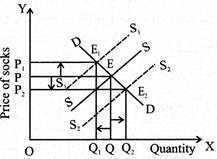

Q.23. How do the equilibrium price and quantity of a commodity change when price of input used in its production changes?

Ans. A change in price of an input will influence the cost of production and hence its supply.

An increase in the price of input will increase the cost of production leading to decrease in supply. The equilibrium price will increase but the equilibrium quantity will fall as a result of decrease in supply.

Similarly, a decrease in the price of input will increase the supply and reduce the equilibrium price though the equilibrium quantity will increase.

The above diagram shows that due to decrease in supply, the supply curve shifts to the left. E1 becomes the new equilibrium point and the price rises from OP to OP1. The quantity demanded falls from OQ to OQ1 and due to increase in supply, the supply curve shifts to the right. E2 becomes the new equilibrium point & the price falls from OP to OP2 and the quantity demanded rises from OQ to OQ2.

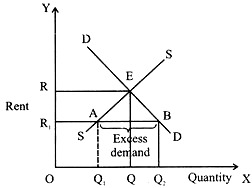

Q.24. Suppose the market demand rent for apartments is too high for common people to afford. If the government comes forward to help those seeking apartments on rent by imposing control on rent, what impact will it have on the market for apartments?

Ans. If the government comes forward and imposes control on maximum rent to be charged for apartments, it will have to be below the equilibrium price OR.

If it is fixed as say OR1, it will lead to:

(i) Excess demand to the extent of Q1Q2

(ii) Black marketing by landlords i.e., they will charge higher rent than what has been fixed by the government, illegally of course.

Q.25. Describe how is price determined in a perfectly competitive market with fixed number of firms.

Ans. Perfectly competitive market accepts the price determined by free forces of demand and supply. Equilibrium price is price at which quantity demanded is equal to quantity supplied. It is at the point where demand and supply curves intersect each other.

Determination of equilibrium price can be understood by the following schedule and diagram:

Q.26. Explain “large number of buyers and sellers” feature of a perfectly competitive market.

Ans. The feature implies that the number of sellers (firms) in the market is so large that no individual seller on its own can influence the market price. It is because the individual seller’s share in the total market supply is negligible.

Also, the number of buyers of the market is so large that no individual buyer on its own can influence the market price. It is because the individual buyer’s share in total demand is negligible.

Q.27. Explain why are firms mutually interdependent in an oligopoly market.

Ans. Firms are mutually interdependent because an individual firm takes decision about price and output after considering the possible reactions by the rival firms.

Q.28. Explain why there are only a few firms in an oligopoly market.

OR

Why is the number of firms small in an oligopoly market? Explain

Ans. The main reason why the numbers of firms are few is that there are barriers which prevent entry of items into industry. Patents, large capital requirement, control over crucial raw materials etc. prevent new firms from entering into industry. Only those who are able to cross these barriers are able to enter.

Q.30. Can you think of any commodity on which price ceiling is imposed in India? What may be the consequence of price ceiling?

Ans. When the maximum price to be charged is fixed by the law it is called price ceiling. Price ceiling is imposed to keep the market price below the equilibrium price. There is price ceiling (or maximum control price) on prices of fuel, sugar, wheat, many medicines etc. Rent Control Act is also an example of price ceiling.

The consequences of price ceiling are:

(i) Excess demand:

Since in price ceiling, price is fixed at a price below the equilibrium price, there will be excess demand.

(ii) Emergence of black market:

Excess demand leads to the black marketing of the commodity and the product is illegally sold at a higher price.

(iii) Rationing due to shortage of supply:

Due to shortage of supply generally rationing is adopted through which fixed quantity is made available to the consumer at fixed price.

Q.31. Explain why the demand curve of a firm under monopolistic competition is negatively sloped.

Ans. In case of monopolistic competition, even though products are different, they are close substitutes of each other. Every seller has monopoly over his product and can decide his own price. However, since a number of close substitutes are available, each product will have an elastic demand curve i.e. it will be downward sloping or negatively sloped.

Q.32. What is the reason for the long run equilibrium of a firm in monopolistic competition to be associated with zero profit?

Ans. I. A firm under monopolistic competition will earn zero profit in the long run because of free entry and exit of firms.

II. If firms are earning super normal profits in the short run, new firms will be attracted to the industry. With the increase in supply, the profits will come down to the level of normal profits only.

III. Similarly if firms are incurring losses in the short nm, some firms will leave the industry and the remaining firm will start earning normal profits.

IV. Thus in the long nm firms under monopolistic competition can not earn super normal profit.

V. Profit really implies super normal profit but normal profit is considered as being just equivalent to the cost of production.

VI. Hence it can be said that the long run equilibrium of a monopolistic firm is associated with zero profit.